How to Get Property Insurance in Japan for Foreigners

Japan has been experiencing a significant increase in non-Japanese property ownership in recent years, due to the depreciation of the yen, attractive real estate market, and opportunities for long-term investment.

Japan has no restrictions on non-Japanese nationals owning property, and the requirements and processes to own property are generally the same as those for Japanese nationals.

However, owning a property is not just about purchasing it; it also involves responsibilities such as insurance, tax, and management.

This article will explain the types of property insurance in Japan, non-resident home insurance, what the types of insurance cover, and tips for choosing the right insurance and reducing costs.

How property insurance works in Japan (government framework explained)

Unlike many countries, Japan’s insurance policies combine private insurance companies, a government-backed earthquake reinsurance program, and strict oversight by the Financial Services Agency (FSA).

Here’s the framework that determines how fire and earthquake insurance work in Japan.

1. Oversight by the financial services agency (FSA)

All insurers operating in Japan—both domestic and foreign—are regulated by the Financial Services Agency (金融庁, kin yuu chou). The FSA oversees:

insurance company licensing

premium setting guidelines

consumer protection

solvency and compliance

dispute resolution and complaints handling

This regulatory structure ensures that policies sold to homeowners remain standardized, transparent, and financially stable—even during major natural disasters.

2. Fire insurance is a private, market-driven product

Fire insurance (火災保険, kasai hoken) is offered through private insurance providers and cooperatives. Premiums differ based on:

building structure (wood, steel, concrete)

age and renovation history

region and natural disaster risk

optional add-ons (flood, water damage, accidental breakage)

Because fire insurance is driven by market competition, coverage varies significantly between insurers, and premiums can differ by tens of thousands of yen depending on the provider and options.

Important: Fire insurance is not mandated by law, but mortgage lenders almost always require it when taking out a home loan.

3. Earthquake insurance uses a government-backed system

Earthquake insurance (地震保険, jishin hoken) is a nationally standardized product. It is jointly provided by:

private insurance companies, and

the Japan Earthquake Reinsurance Company (JER), a government-backed organization.

This means:

premiums are set within regulated national ranges

terms and coverage limits are standardized across the country

claims are processed the same way regardless of insurer

the government supports payouts for large-scale disasters

This standardized structure exists because Japan is one of the most earthquake-prone countries on Earth—and private insurers would struggle to absorb losses alone.

4. Fire insurance and earthquake insurance must be purchased together

Earthquake insurance cannot be purchased as a standalone product. It must be added as a supplement to a fire insurance policy.

Key structural rules:

Earthquake insured amount must be 30%–50% of fire insurance’s building/contents coverage

Maximum payout is capped, based on government guidelines

Claims follow the standardized “Total Loss / Half Loss / Partial Loss” damage categories

Premiums vary by region, building type, and time period

Because the system is regulated, the cost of earthquake insurance in Tokyo will be the same regardless of which insurer you choose—as long as the building and coverage are identical.

Property insurance challenges for non-residents

Resident and non-resident foreign property owners in Japan face the following unique challenges when getting property insurance.

1. Complex insurance system

Japan has a complex insurance system, and choosing the right plan can be challenging. The type of insurance and insurance premiums vary greatly depending on individual needs.

2. Language barrier

Understanding local laws and regulations and the terms of insurance policies written in Japanese can be very difficult. The language barrier often prevents foreign property owners from choosing the optimal insurance plan, which can lead to significant problems.

3. Requirements for non-Japanese nationals

Some insurance agents require an emergency contact person who resides in Japan and a domestic phone number.

One customer shared their experience trying to get homeowners' insurance as a non-resident: “I originally tried going through a local agent in Japan, but they required a Japanese phone number, which I can't get without residency.”

👉 Read more about Javier Batista Santiago's story of getting a house in Japan.

4. Insurance bills and notifications

For non-resident property owners, receiving insurance bills and notifications sent to their Japanese property can be challenging. Note: Many non-resident property owners use MailMate, a virtual mailbox service that uploads all incoming mail into a cloud account. The service also provides a bill pay service so that property owners can stay on top of insurance premiums.

Types of homeowners' property insurance in Japan

Event |

Fire Insurance |

Earthquake Insurance |

Notes |

Fire |

✔️ |

❌ |

Unless caused by earthquake |

Flood |

✔️ |

❌ |

Depends on policy type |

Typhoon |

✔️ |

❌ |

Included in most plans |

Earthquake |

❌ |

✔️ |

Requires add-on |

Landslides |

Sometimes |

✔️ |

Risk-dependent |

Theft |

✔️ |

❌ |

Often included |

In Japan, there are two main types of property insurance: fire insurance (火災保険 - kasai hoken) and earthquake insurance (地震保険 - jishin hoken).

1. Fire insurance

A typical fire insurance policy, known as 火災保険 (kasai hoken), is a general home insurance. Despite the name, fire insurance in Japan also covers property damage caused by natural disasters, such as typhoons, floods, water leaks, snow damage, lightning strikes, heavy rains, theft, and other unintentional accidents.

Inside a fire insurance plan, you can purchase protection for two categories: building coverage and household contents coverage.

Building coverage—The primary purpose of fire insurance is to cover damages to buildings caused by fire hazards and various types of natural disasters. However, building damage caused by disasters is typically only covered if the building is repaired every 10 years. Therefore, it is important to maintain regular upkeep and retain proof of any building repairs.

Household contents coverage—Fire insurance also covers damage to household goods caused by natural disasters and theft. Many insurance plans offer additional coverage for accidental damage to household contents for an extra fee.

2. Earthquake insurance

The purpose of earthquake insurance is to stabilize the livelihoods and provide financial protection for those affected by earthquakes. The policyholder is required to set the insured amount for earthquake coverage within a range of 30%-50% of the amount of insurance provided by his or her fire insurance.

Earthquake insurance can be relatively expensive, while serious earthquakes occur infrequently. However, when earthquakes do occur, they often cause extensive damage. Purchasing earthquake insurance is highly recommended if your budget allows.

Average cost for fire and earthquake insurance (homeowner's property insurance) in Japan

The average price Japanese consumers pay for fire insurance and annual earthquake insurance premiums for a detached house in Japan is approximately ¥50,000 ($340) for a year, according to insurance company Minbaku.

Your insurance premium will depend on factors such as the age and condition of the building, the construction type, whether you choose coverage for special circumstances, desire additional services, whether you desire coverage for household goods, etc.

Property Type |

Building Coverage |

Contents Coverage |

Combined Total |

60m² Concrete Apartment (Tokyo) |

¥12,000-18,000 |

¥8,000-12,000 |

¥20,000-30,000 |

100m² Wooden House (Rural) |

¥25,000-40,000 |

¥10,000-15,000 |

¥35,000-55,000 |

120m² Concrete House (Urban) |

¥18,000-30,000 |

¥12,000-18,000 |

¥30,000-48,000 |

Note: These figures are estimates and actual costs will vary based on specific property details and coverage options.

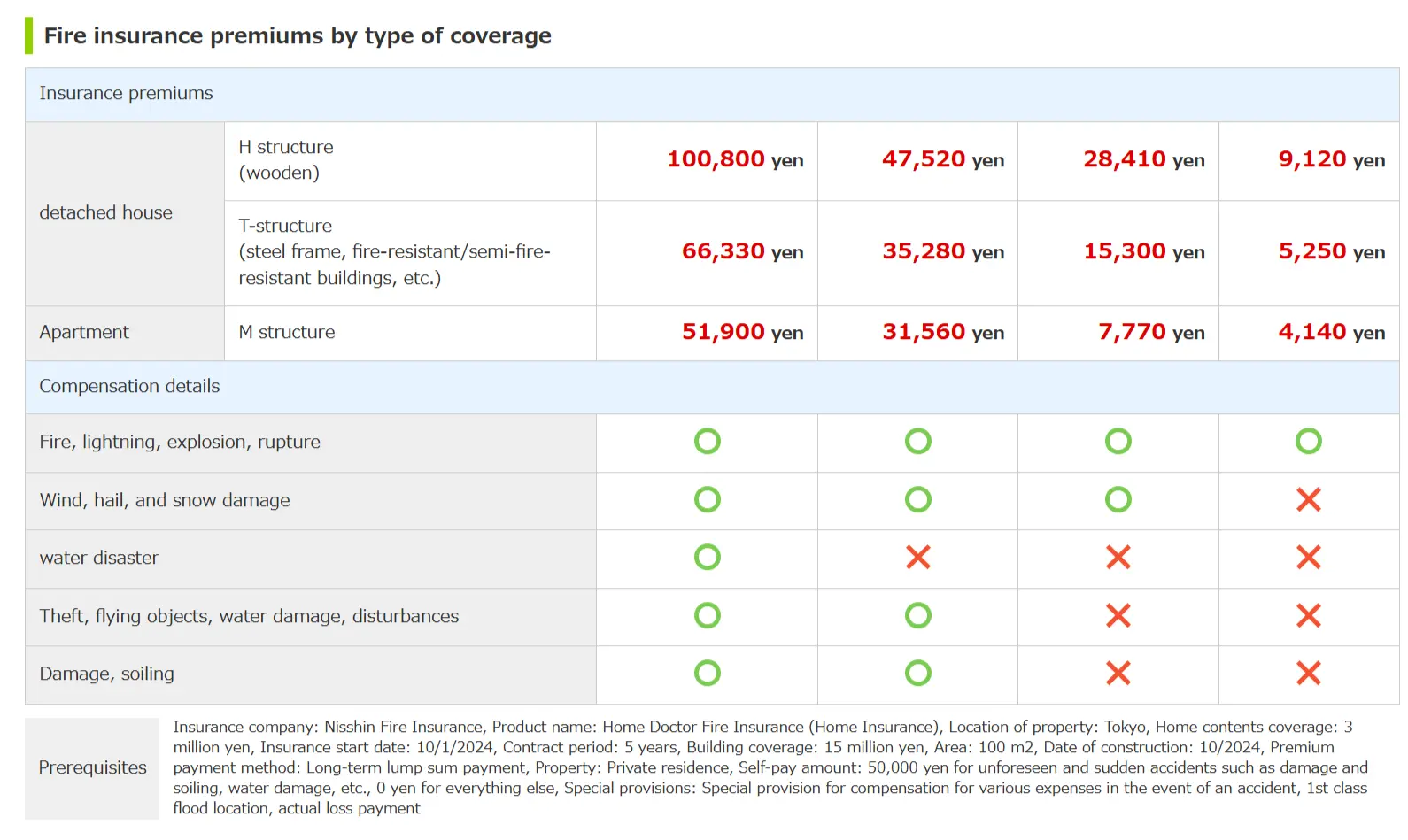

Here's a chart from Kakaku.com, a popular price comparison site in Japan, showing current prices for various property insurance plans depending on building type.

Wooden detached houses (H structure) command the highest premiums at approximately ¥100,800 ($692) for comprehensive fire and explosion coverage—reflecting their higher vulnerability to fire damage.

In contrast, steel-frame and fire-resistant buildings (T-structure) benefit from substantially lower rates (¥66,330; $455) for the same coverage, representing a 34% reduction. Apartment buildings (M structure) offer the most economical rates at ¥51,900 ($356) for primary fire coverage, nearly half the cost of wooden houses.

This pricing structure directly corresponds to statistical risk assessments: wooden structures historically suffer more extensive damage and total losses in fire incidents compared to concrete or steel-framed buildings.

The premium differentials become even more pronounced for secondary coverages like water damage, where wooden houses cost nearly four times more to insure than apartments.

Factors to consider when shopping for property insurance in Japan

After reviewing many insurance plans and policies, here's what we recommend that you consider when looking to purchase fire or earthquake insurance.

1. Customer service

Insurance terms and claims are often only provided in Japanese. So look for an insurance company that provides support in English or that has a track record of assisting foreign residents.

2. Coverage and cost

When considering comprehensive fire insurance coverage, many insurance plans in Japan include protection for personal accidental damage as well. For instance, coverage may extend to situations like a child accidentally breaking a TV while playing, or accidentally spilling red wine on a carpet.

However, basic plans do not include personal accidental damage coverage. Additional or all-inclusive plans tend to be more expensive.

Additionally, even if a basic insurance plan includes flood coverage, they might have strict conditions. For example, some policies only cover flood damage if the water level rises at least 45cm above ground level. This means that damage to a basement will not be covered, even when flood damage is otherwise included. The greater the coverage, the higher the cost. It is essential to assess the risks specific to your property and select a policy that provides sufficient protection without unnecessary extras.

When choosing fire insurance, it is crucial to check the terms and conditions to understand what is covered and to determine whether a basic or comprehensive plan is more suitable for your needs.

Some individual policies may or may not include coverage of buildings used for commercial purposes, e.g., short term rentals or stores, so you may need to purchase a separate policy if you wish to purchase insurance for an income-generating property.

3. Contracts and claims

Carefully review the terms and conditions of the insurance policy, including the claims process. Make sure that the insurer has a clear and straightforward claim procedure, and examine the deductibles and exclusions that could impact your coverage.

Damage Level |

Description |

Payout Percentage |

Total Loss |

Building collapse, structural damage exceeding 50%, or complete submersion |

100% of coverage limit |

Half Loss |

Damage between 20-50% of building value |

50% of coverage limit |

Partial Loss |

Damage between 3-20% of building value |

5% of coverage limit |

4. Benefits and limits

Understand the maximum amount of coverage limits for the insurance plan, and ensure they align with the actual cash value or replacement cost of your property.

Comprehensive guide on how to reduce property insurance costs

Here are some actions to consider if you're looking to reduce your insurance premiums and choose insurance products that will provide you with the amount of coverage you are hoping for.

1. Opt for named perils coverage

Choose an insurance plan that covers specific risks instead of comprehensive insurance. This can reduce costs if you are confident that certain risks are unnecessary for the property.

2. Avoid over-insuring

Ensure your coverage aligns with the actual cash value or replacement cost of your property and contents. It is important to avoid over-insuring the property's worth.

3. Choose the optimal insurance for your needs

Choose an optimal insurance plan tailored to your specific type of property. For example, if you own a high-rise building (referred to as a “mansion” in Japanese), many insurance companies offer a “mansion plan” that excludes unnecessary risk coverage specific to high-rise buildings. Choosing the right insurance plan for your property needs can help reduce overall costs.

4. Appoint bilingual professionals

Enlisting professional assistance is highly recommended. MailMate works with an insurance company and has helped many non-resident property owners get fire insurance and earthquake insurance.

They work with you through the risk assessment process, provide English explanations for all the Japanese insurance terms, and will help you understand payout costs and coverage limits.

Types of Japanese insurance providers: Insurance company vs. cooperative insurance

There are two main types of property insurance providers in Japan: an insurance company (保険会社 - Hoken Gaisha) and a cooperative insurance (共済 - Kyosai).

A cooperative (Kyosai) is a non-profit organization established voluntarily by a group of people who aim to improve their lives through shared resources.

Cooperative insurance operates as a mutual aid system, where members share their premiums to establish a collective fund. This fund is used to provide financial support during unexpected contingencies, compensating for financial deficits and stabilizing the lives of members and families.

Cost: Cooperative fire insurance is significantly less expensive than insurance from an insurance company.

Coverage: The coverage provided by cooperative insurance is limited compared to that offered by insurance companies.

Conversely, insurance companies typically offer broader coverage, but their plans are more expensive.

How to use MailMate to solve insurance and property management issues

MailMate can help you set up property insurance and act as an emergency contact for non-resident foreign property owners.

Not only does MailMate provide bilingual contract support for foreign property owners looking to purchase homeowner's insurance, but MailMate also provides comprehensive property management services, making it an ideal solution for managing properties in Japan from overseas.

Aside from home insurance, MailMate also provides the following:

Receive and pay your property tax and insurance bills without a Japanese bank account.

Register MailMate as your Domestic Point of Contact at the time of your property purchase.

Receive your Japanese Mail digitally with English summaries & an interactive Mail Concierge.

Local point of contact and bill pay for your condo or building association.

Local point of contact for utility set-up and ongoing bill-pay.

Get fiber optic internet set-up at your property (inclusive of monthly internet fees)

The service also includes handling mail through a virtual address, forwarding received mail, and providing translation services when needed.

Frequently asked questions

Is property insurance mandatory in Japan?

Property insurance is not legally mandatory in Japan. However, banks and mortgage lenders almost always require fire insurance when issuing a home loan. Earthquake insurance is optional but highly recommended.

Do I need earthquake insurance for my property in Japan?

Earthquake insurance (地震保険) is strongly recommended, especially in high-risk areas like Tokyo, Osaka, and Kanagawa. Standard fire insurance does not cover earthquake damage, so without earthquake coverage, you may have no financial protection after a major quake.

Can non-residents buy property insurance in Japan?

Yes. Non-residents can purchase both fire and earthquake insurance. Many insurers require a Japanese phone number, a domestic emergency contact, and the ability to receive mail in Japan. Non-residents often use bilingual representatives or property management services to handle insurance communication and payments.

How do I file a property insurance claim in Japan?

To file a claim, contact your insurer immediately after damage occurs, submit photos and repair estimates, and allow the insurer to inspect the property. Claims are assessed as Total Loss, Half Loss, or Partial Loss. Non-residents can appoint a local representative to manage documentation and communication. Claims should be filed as soon as possible, especially after natural disasters.

In closing

Owning property in Japan as a non-resident foreign national comes with unique challenges. Choosing the right property insurance is a key part of the process.

By understanding your insurance options, reducing unnecessary costs, and partnering with bilingual professionals, you can streamline property management and enjoy the benefits of owning property in Japan with peace of mind.

Spending too long figuring out your Japanese mail?

Virtual mail + translation services start at 3800 per month. 30-day money-back guarantee.